Trade policy and inflation risks

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

Although the administration has expressed support for a lower federal funds rate, several policy developments since taking office continue to complicate that objective. In particular, recent tariff actions – some of which were legally challenged and later invalidated by the Supreme Court – have contributed to ongoing uncertainty around trade policy. Subsequent temporary tariff measures, even if intended as interim steps, may shape expectations for future policy direction.

Even if tariffs are refunded, the impact of policy uncertainty may linger. Businesses respond cautiously when policies appear unsettled, particularly when they increase input costs. In 2025, similar uncertainty contributed to slower hiring and a deceleration in employment growth. A comparable response in 2026 cannot be ruled out, particularly if firms face cost pressures and limited visibility into future policy.

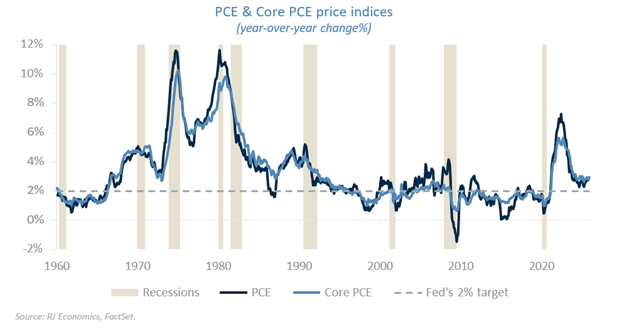

Tariffs have delayed the return to 2% inflation

The fundamental issue is that tariffs push prices, and therefore inflation, higher. Absent the 2025 tariff wave, inflation would likely be at, or even below, the Fed’s 2% target, giving policymakers room to bring the funds rate closer to the Fed’s long-run neutral rate of ~3%. Instead, the administration is insisting on much larger rate cuts while simultaneously enacting policies that make disinflation harder.

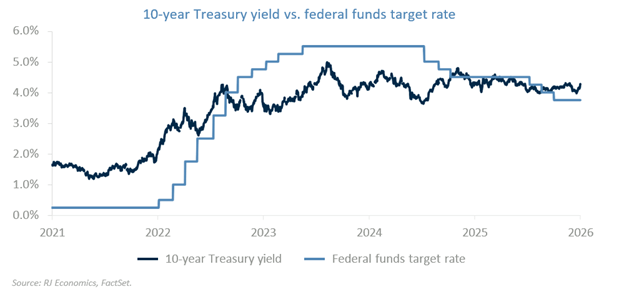

Comments from several administration officials reveal a basic misunderstanding of the mechanics of interest rates. The Fed controls only one rate: the overnight federal funds rate. Every other rate – mortgages, business loans, the 10-year Treasury yield – is set by markets, not the central bank.

Since September 2024, the Fed has cut the funds rate by 175 basis points, yet the 10-year Treasury yield remains stuck near 4.25%. Markets simply do not believe inflation is coming down sustainably. As long as inflation expectations remain elevated, lowering the funds rate will not bring down long-term rates, rendering political pressure on the Fed largely pointless.

Geopolitical shocks are now adding fuel to the fire

The ongoing conflict involving Iran has sharply lifted petroleum and gasoline prices. While analysts often note that the Fed can “look through” temporary spikes in energy prices, that is only true if core inflation remains stable.

Historically, such as before the Great Recession, headline inflation accelerated while core inflation remained contained, giving the Fed room to wait. However, today’s circumstances are different. Given the administration’s expansionary fiscal stance, especially the large tax refunds scheduled under the One Big Beautiful Bill Act, aggregate demand is poised to improve. That increases the likelihood that both headline and core inflation will rise concurrently, forcing the Fed to remain cautious.

Why rate cuts are unlikely anytime soon

Fed officials will not risk lowering interest rates until they are confident that any rise in headline inflation is not spilling into core measures. Markets will also continue to push long-term interest rates higher if they perceive inflation risks worsening. In this environment, cutting rates simply because the administration desires lower borrowing costs is unrealistic.

Bottom line

The Fed may set the federal funds rate, but markets ultimately judge whether policy is on the right path. If investors believe the Fed, constrained by the administration’s tariff and fiscal choices, cannot credibly achieve 2% inflation, they will keep long-term interest rates elevated. That message will be loud and clear, regardless of the administration’s preferences.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.